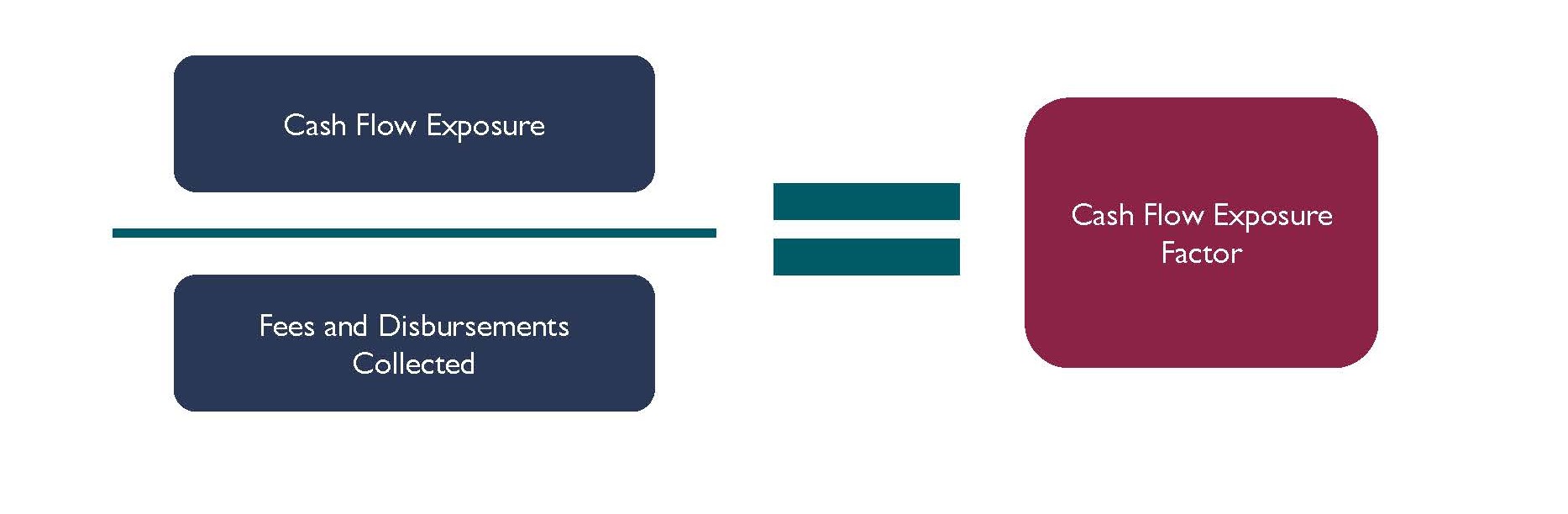

It can be useful in managing cash flow to monitor work done for which you have not been paid, including work in progress (WIP), unbilled disbursements and accounts receivable (AR). This is your cash flow exposure. Dividing the month's cash flow exposure by the amount of fees and disbursements collected will give you a cash flow exposure factor.

Monitoring trends in your cash flow exposure factor can give you important information about the speed of the cash flow cycle in your practice. A lower exposure factor evidences a lower gap between investment and collection.

Your target cash flow exposure factor will depend on the nature of your practice:

- A contingency practice has a very high WIP exposure because fees are not billed until the matter is resolved. However, there should be no AR exposure since bills are paid from settlement proceeds.

- A transactional practice will typically have a volatile short-term WIP and unbilled disbursement exposure but should have low AR exposure because files are billed and collected when the transaction closes.

- A civil litigation practice that bills monthly should be able to keep its WIP and unbilled disbursements exposure to a minimum; AR exposure will depend on how quickly the practice’s clients pay.

Generally, the lower your exposure factor, the better. To keep your exposure factor low, it helps to:

- Only take unpaid work if you consciously decide to provide those services pro bono.

- Take steps to ensure payment. If you have a trust account, a strong retainer policy can be critical. If you bill after services are provided, this may be a matter of assessing a client's willingness and ability to pay before taking on their matter, and maintaining the relationship so that they are motivated to pay promptly.

- Bill WIP as soon as possible.

- Keep unbilled disbursement to a minimum.

- Pursue payment for AR promptly.

A Note on Borrowing – Rarely a Borrower Be!

Managing debt is a key part of cash flow management. Your accountant can advise on options for financing your practice and the risks and benefits of different forms of credit for your business.

As your firm matures, you will have to consider from time to time whether to incur new debt. Sometimes borrowing money will be a sensible decision but in a mature firm the need to borrow is sometimes a sign of trouble.

Generally, the less you borrow and the quicker you pay off your debts, the healthier your practice will be. If you use credit conservatively you will have a better chance of building a sound, financially secure practice. A conservative approach to credit includes:

- paying all credit card, overdraft and trade credits in full each month;

- financing capital assets from cash flow whenever possible. If you do borrow to finance capital assets, structure your payments so the debt is reduced faster than the assets are used up. If you can’t afford the payments, don’t make the purchase; and

- debt always takes priority over draws. Rather than borrowing to pay yourself, trim your personal needs to match your income.

A conservative approach to credit helps ensure more stable and secure draws in the long run. It also supports your ability to focus on practising law without the distraction and pressure of financial worries.

When the client has limited resources – avoid the road paved with good intentions

When a client has limited resources, your desire to help can quickly lead to a cash flow management problem. It can be tempting to try and help the client and alleviate cash flow problems from unpaid AR by using a line of credit or otherwise borrowing funds to keep the practice going while awaiting payment.

Over-reliance on a line of credit will see you paying the bank more than you pay yourself for extended periods of time. If you limit your use of a line of credit to financing AR you are guaranteed to recover, such as settlement proceeds, and pay the line of credit off as soon as the money comes in, it can be a useful tool to manage cash flow.

If you have a few tight cash flow months, it can be tempting to use a line of credit to smooth those out. That can see you moving deeper into debt each day. Before adding to your debt load on the line of credit, consider:

- eliminating unnecessary overhead;

- focusing on work that you can bill and collect quickly (without neglecting commitments to other matters); and

- reducing your draws.